TopComm wrote:Did some tweaking for a little better 7σ with 16198 - Lowest return: 25.99

Oh nice work! I like this one.

Moderator: Aitrus

TopComm wrote:Did some tweaking for a little better 7σ with 16198 - Lowest return: 25.99

Octjan2 wrote:This may be the best one yet. However, there is a lot of time in F.

onerepmax wrote:there are several great strategies with less than 2 months (15% time) in F

http://tspcalc.com/seasonal.php?ID=1619 ... =5&Fmax=15

HINT: Don't use 2017 in your sort yet. I think the incomplete yearly data skews it enough to miss out on some nice numbers.

I'll be transitioning to #16013 soon, either at the first of the year or next IFT (only 1 day difference)

fordest wrote:In case you missed it in the other thread, I found a sigma of 10.1!

16250

We need updated charts 12X12...

And I don't get the math but I love reading the explanations. What does that mean for likelihood of a negative return?

fordest wrote:In case you missed it in the other thread, I found a sigma of 10.1!

16250

We need updated charts 12X12...

And I don't get the math but I love reading the explanations. What does that mean for likelihood of a negative return?

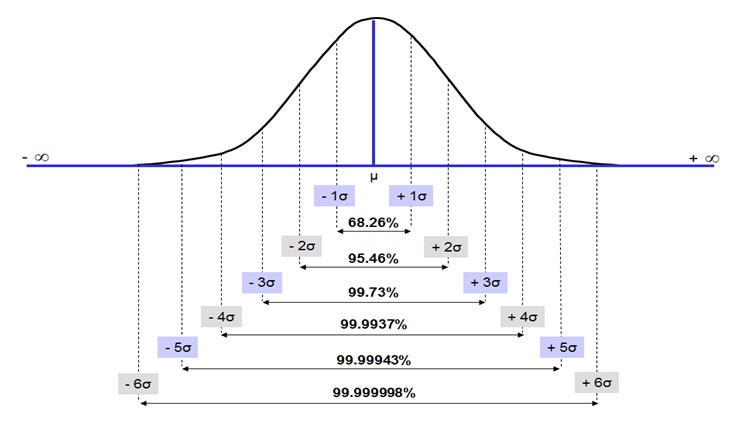

12squared wrote:The term "sigma" is used in the world of Quality Control as a metric of reliability. It is akin to the use of the decibel (dB) for sound and radio signal levels, in which ratios span great ranges, e.g. from micro to giga. Reliability is usually expressed as a 1 in a______ chance of defects. In the context of annual returns, I defined the defect limit as the 0% return, because anything less results in "loss of capital".

The relative reliability of sigmas was calculated by dividing their respective Cumulative Normal Distributions obtained from Excel's NORMDIST function.

Hi everyone! Been on here for a little while but have never posted.fordest wrote:In case you missed it in the other thread, I found a sigma of 10.1!

16250

We need updated charts 12X12...

And I don't get the math but I love reading the explanations. What does that mean for likelihood of a negative return?

Wow. Mine too...... and the lowest year: 26.93% Thanks for pointing this one out.Sad Al wrote:Whoever came up with strategy #24823, you are my hero. Mean 30.12, standard deviation 1.78%. Ratio 16.92.

12squared wrote:hmarkway wrote:So using your example, if the Mean/StdDev is 2.0, it is 99% likely that no more than 1.98 years out of 20 (20*0.099) will be negative, but at least (>0%) 0.456 years out of 20 (20*.0228) will be negative. Am I looking at this the correct way?

12squared wrote:Yes you are. In whole numbers, 1 year out of 40, the same as the the mean-2SD value.

| Fund | Price | Day | YTD |

| G | $18.19 | 0.01% | 1.24% |

| F | $18.58 | -0.32% | -3.33% |

| C | $79.08 | -0.21% | 6.34% |

| S | $76.95 | -0.41% | -0.18% |

| I | $40.73 | -0.98% | 1.37% |

| L2065 | $15.67 | -0.50% | 3.66% |

| L2060 | $15.67 | -0.50% | 3.67% |

| L2055 | $15.68 | -0.50% | 3.67% |

| L2050 | $31.50 | -0.44% | 2.93% |

| L2045 | $14.38 | -0.41% | 2.81% |

| L2040 | $52.59 | -0.38% | 2.72% |

| L2035 | $13.91 | -0.35% | 2.60% |

| L2030 | $46.37 | -0.32% | 2.50% |

| L2025 | $12.95 | -0.18% | 1.90% |

| Linc | $25.31 | -0.14% | 1.64% |